Risk Management Guide for Small Businesses

Risk management refers to the process of identifying, evaluating and responding to risks that would have adverse effects on your business. The risks could be caused by both external and internal factors. Business owners should understand that they can be met with risks regardless of the nature of their business and it’s size. Moreover, the risks that they face can have a varying impact on their business operations. This could challenge their business’s long-term viability.

What is risk management?

Risk management is a company’s way to prepare for the worst and to mitigate any unforeseen event. Which could have a negative impact on the company resources and expenditures.

The International Organization for Standardization under ISO 31000:2018 lists guidelines for risk management. Every business should try to work inline with to make sure their business is risk ready.

You may hire or speak to a skilled accountant or risk manager. They can help you mitigate the financial risks that your small business can potentially face. Building a risk management plan as part of your company’s strategic planning can help plan for and mitigate these risks. If you do not make strategic plans for your company, you might want to review and enlist our strategic planning services.

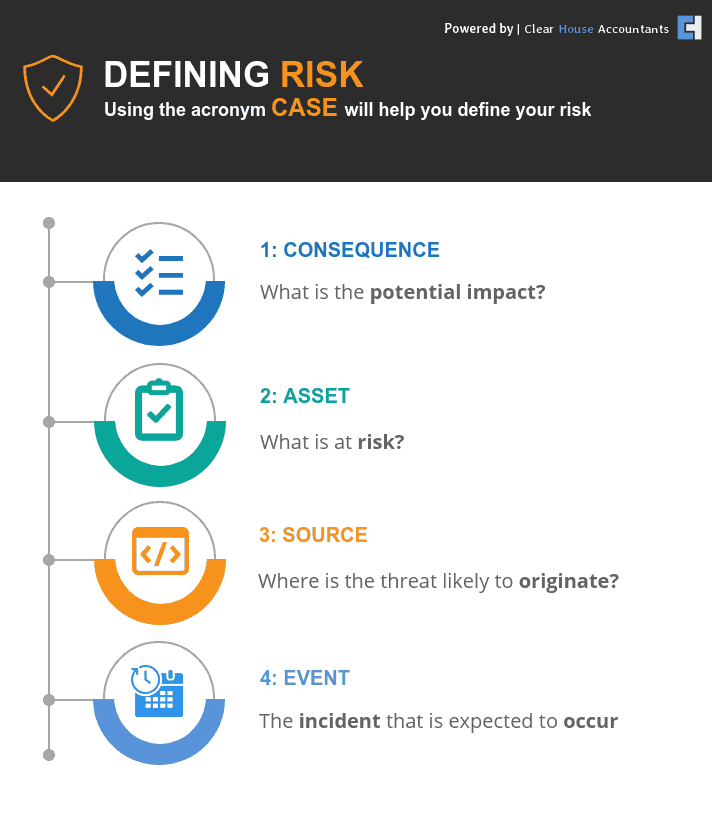

What are the major risks faced by businesses?

Business owners must have a strategy that helps them identify risks. They should also follow a step-by-step approach that helps them define the business risks that they might come across in the future. The outline shown below is a general approach used by small businesses to identify business risks.

Business owners should be well aware of the risks they might face — before they can actually develop a risk response strategy. We have defined 5 major risks that business owners may face that may prevent them from achieving their goals.

- Strategic Risk: They are directly aligned with your company’s strategy. Strategic risks can prevent a business from achieving its goals. They may be caused by poor strategic planning or due to erroneous execution. A skilled small business accountant in London can help you design a comprehensive and well-thought-out business strategy that will help you mitigate or avoid this risk.

- Compliance Risk: If your business is not in compliance with all the necessary laws and regulations then your business may face a compliance risk. It can even occur if your business has been expanding and you have stopped keeping track of the compliance measures. Finding an accountant with suitable compliance expertise can ensure the safety of your business.

- Financial Risk: This type of risk refers to the potential for a sudden financial loss in terms of money. This could be cash flowing into and out of your business. The risk of this happening can be high in certain situations. For example, when a business depends on a single client for a large proportion of their revenue or when the business has accumulated too much debt. Financial risks are the most tricky to deal with as they can impact payments to suppliers or employee payroll.

Our guide to cash flow forecasting can help you predict and plan for such issues.

Video: The Ultimate Risk Management Guide

A risk management plan ensures that risks are managed properly. The goal is to reduce the impact of negative risks and to increase the impact of opportunities. Watch our video to learn more.

Related: Your business might be vulnerable to substantial financial losses due to the COVID-19 lockdown. Stay updated on how you can protect your business during these uncertain times through our Coronavirus Support Hub.

- Operational Risk: Sometimes businesses are so worried about external issues that they are unable to come up with a well-defined risk management plan to take care of potential in-house operational issues. These risks could include failures of your day-to-day operations, technical failures, or staffing issues. Although this type of risk might seem minimal in comparison to other risks. However, the operations of a business are at its core. It is worth protecting them using an in-depth scenario planning methodology or by using other strategic methods.

- Reputational Risk: No matter how big or small your business is, business reputation is vital to any ongoing businesses success. Reputational damage can lead to loss of revenue, loss of business partners and loss of clients along with staffing issues. It is crucial to have an effective business strategy in place that could guard you against this risk. Hiring the right accounting firm, employees, directors and a good marketing agency will help you minimise this risk. You might want to read our guide on effective hiring to help you hire the best talent and in turn, reduce your employee turnover risk.

What is a risk management plan and why do you need it?

A risk management plan helps you develop a detailed strategy to deal with certain risks that are particularly important for your businesses’ success. Your risk management strategy must incorporate factors like time and resources.

How to create an effective risk management plan?

A risk management plan requires one to follow a methodological four-step approach as explained below:

1.Identify

The first and most important step of creating a risk management plan is to identify potential risks that are related to your business. You can start with a brainstorming session with your team members and define categories for the risks that are relevant to your business. Once you have identified all the risks, they should be categorically placed in a document known as the Risk Register.

Find an accounting firm nearby that specialises with risk management. You can also find a risk consultant to help you identify risks your business is most vulnerable to. These steps can help you prepare a comprehensive risk management plan accordingly.

2. Assess

The next step would be to analyze and assess the different risks that you have categorized in the first step. Risks are usually assessed based on the product of two factors. These are their likelihood of occurrence and the level of impact they have on your business. Generally, the risk assessment results are stored in the form of a matrix. A matrix gives the project manager a wholesome idea about what the risks are and how they may impact the project.

You can utilize our risk matrix template available here.

3. Manage

The next step is to manage the risks identified or in other words to decide on a relevant response for them. An appropriate and cost-effective risk response strategy needs to be developed for each risk. Some of the most common risk response strategies are listed below.

Risk response strategies

- Avoid

- Mitigate

- Transfer

- Accept

- Escalate

4. Monitor and review

This process comes in when your risks have been identified, analyzed and a response strategy has been developed. You will then need to develop an effective mechanism. This should allow you to monitor the risks and ensure that they are controlled at an early stage. You must discuss your risk management plan with your insurance company to help plan your coverage accordingly. Our guide to insurance can help you plan effectively to prepare for the potential risks your business faces.

Source : Medium.com – Mahzeb Monica (Link)